- SovereignBeat

- Posts

- Fed keeps the market on its toes

Fed keeps the market on its toes

will we see the cuts — and a market rally?

In partnership with

Welcome back to SovereignBeat!

No Fed cut, but markets bounce with the relief

U.S. data mixed—no clear signal and ongong uncertainty

ECB, BoE, Riksbank on hold; SNB cuts.

Europe up 14% YTD vs. S&P down 3%.

Euro steady at 1.09 despite tariff threats.

Let’s dissect

We Also Recommend

Apple's New Smart Display Confirms What This Startup Knew All Along

Apple has entered the smart home race with its new Smart Display, firing a $158B signal that connected homes are the future.

When Apple moves in, it doesn’t just join the market — it transforms it.

One company has been quietly preparing for this moment.

Their smart shade technology already works across every major platform, perfectly positioned to capture the wave of new consumers Apple will bring.

While others scramble to catch up, this startup is already shifting production from China to its new facility in the Philippines — built for speed and ready to meet surging demand as Apple’s marketing machine drives mass adoption.

With 200% year-over-year growth and distribution in over 120 Best Buy locations, this company isn’t just ready for Apple’s push — they’re set to thrive from it.

Shares in this tech company are open at just $1.90.

Apple’s move is accelerating the entire sector. Don’t miss this window.

Past performance is not indicative of future results. Email may contain forward-looking statements. See US Offering for details. Informational purposes only.

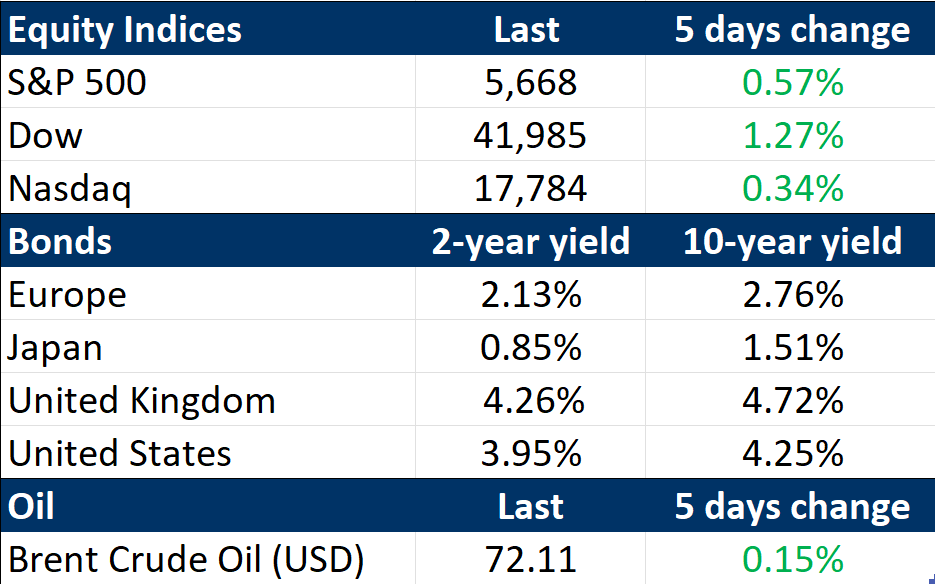

Markets Snapshot

As of 21/03/2025 market close

Macro and Fixed Income Markets

US : The focal point of the week’s economic developments came on Wednesday, when the Federal Reserve concluded its March policy meeting. As anticipated, the Fed maintained its benchmark interest rate at 4.25%–4.5%. Officials also reaffirmed their outlook for 50 basis points of rate cuts in 2025, in line with their December projections. However, the updated forecasts included an upward revision to inflation expectations for 2025 and a downward adjustment to projected GDP growth. The Fed also acknowledged rising uncertainty in the economic outlook.

Despite these mixed signals, the overall market reaction was positive. Fed Chair Jerome Powell emphasized that the economic impact of tariffs is expected to be transitory and that longer-term inflation expectations remain anchored near the 2% target. Investors responded favorably to the Fed’s dovish tone, with major equity indexes closing higher on the day.

Economic data painted a mixed picture of the economy last week. On Monday, the Census Bureau reported that retail sales in February rose just 0.2%, falling short of expectations for a 0.7% gain. In addition, January’s figure was revised lower to a 1.2% decline from initial decline of 0.9%—the sharpest drop since July 2021. However, the control group component of retail sales, which excludes volatile categories such as autos and restaurants and is a key input for GDP calculations, rose 1.0% in February, beating the projected 0.4% increase. Also on Monday, the Empire State Manufacturing Survey pointed to weakness in the manufacturing sector. The report showed a significant decline in business activity in March and noted that business sentiment continued to deteriorate for the second month in a row.

In contrast, housing market indicators were more encouraging. Existing home sales rose 4.2% in February, surpassing expectations and supported by an increase in supply. Meanwhile, housing starts for the month came in at an annualized rate of 1.5 million, up 11.2% from January. Despite the month-over-month improvement, the figure was still 2.9% below the level from a year earlier.

U.S. Treasuries delivered gains heading into Friday, with yields falling across most maturities in the aftermath of the Federal Reserve’s policy announcement. Municipal bonds also recorded positive returns for the week, showing resilience despite a high volume of new issuance.

An upcoming PCE inflation report, set to be released on Friday, may help clarify the recent uncertainty surrounding the direction of inflation. In January, the PCE price index rose at an annual rate of 2.5%, a slight moderation from December’s 2.6% reading, suggesting some easing in price pressures.

Europe: Recent monetary policy updates reflected growing trade-related uncertainty, as central banks weighed the risks of slowing growth against persistent inflation concerns,signaling a more data-dependent, wait-and-see approach.

The Bank of England left its policy rate unchanged at 4.5%, as expected. However, only one of the nine members voted for a cut—contrary to market expectations of a more dovish 7–2 split—sending a hawkish signal. Policymakers highlighted elevated inflation expectations as a concern.

Sweden’s Riksbank also held rates steady at 2.25%, following inflation data that remained above target. Governor Erik Thedéen stated that the benchmark rate would likely remain unchanged through early 2028, though the bank remains prepared to respond if conditions shift.

In contrast, the Swiss National Bank took a more dovish turn, lowering its policy rate by 25 basis points to 0.25%. The decision was attributed to subdued inflation pressures and growing downside risks. SNB President Martin Schlegel noted that additional rate cuts were not anticipated in the near term.

The euro held steady around USD 1.09 throughout the week, hovering near its highest level since November 5, following the German parliament’s approval of a substantial increase in government borrowing. The package includes a major revision of the country’s debt framework—exempting defense spending from debt limits—and outlines a €500 billion infrastructure investment plan. The proposal now awaits a vote in the Bundesrat.

ECB: In remarks to the European Parliament, ECB’s President Christine Lagarde emphasized the need for continued vigilance in light of growing trade-related uncertainties. She warned that a proposed 25% U.S. tariff on European imports could reduce eurozone economic growth by 0.3 percentage points in the first year, with the impact potentially rising to around 0.5 percentage points if the EU were to implement reciprocal measures. Lagarde also noted that inflation could increase by approximately 0.5%, driven by retaliatory tariffs and a weaker euro. Meanwhile, market participants have reduced expectations for European Central Bank rate cuts, now anticipating just two reductions—likely in April and June—with rates no longer expected to fall below 2%.

Equity Markets

US: U.S. equity markets experienced a week of modest fluctuations, ultimately ending with slight gains that helped recover some ground following the prior week’s dip, which had pushed the S&P 500 into correction territory. By Friday’s close, the S&P 500 rose 0.5% for the week, halting a four-week losing streak. The Dow Jones Industrial Average advanced 1.3%, while the Nasdaq Composite edged up 0.3%.

Despite the broader market’s recovery, the information technology sector—and several of the so-called “Magnificent Seven” stocks that have driven much of the market’s momentum in recent years—underperformed. The tech sector remains down over 9% year-to-date, a stark reversal from its nearly 37% surge in 2024.

U.S. corporations significantly increased their share repurchase activity in 2024, spending nearly 19% more than in the previous year. According to S&P Dow Jones Indices, S&P 500 companies executed a record $943 billion in buybacks last year, up from $795 billion in 2023. On a quarterly basis, repurchases rose 7% in the fourth quarter of 2024 compared to the third quarter.

Europe: The main equity index ended the week relatively flat but continued to significantly outperform its U.S. counterpart, the S&P 500, on a year-to-date basis. The index posted a modest weekly gain, bringing its year-to-date return to approximately 14%, compared to a 3% decline for the S&P 500 over the same period.

In Motion

Read The Daily Upside. Stay Ahead of the Markets. Invest Smarter.

Most financial news is full of noise. The Daily Upside delivers real insights—clear, concise, and free. No clickbait, no fear-mongering. Just expert analysis that helps you make smarter investing decisions.

Thank you for checking out the latest SovereignBeat newsletter! Share your thoughts on the topics covered and let us know if there's anything specific you'd like us to explore.

Read our other publications here

Our Further Reading Recommendations

Ukraine-US Talks Start in Riyadh, Russia-US Meeting to Follow (Bloomberg)

Reply